Update on Navy Federal Scandal: Addressing Racial Discrimination in Home Mortgage Practices

- Joeziel Vazquez

- Dec 23, 2023

- 7 min read

This update is brought to you by Credlocity, the fastest-growing credit repair company in the United States, led by CEO Joeziel Vazquez, a staunch defender and advocate of minority rights in the financial and fintech arena.

Introduction

In recent news, Navy Federal Credit Union, the largest credit union in the United States, has come under fire for alleged racial discrimination in its home mortgage practices. Multiple class-action lawsuits have been filed against the institution, accusing it of denying home loans to Black borrowers at a significantly higher rate than their white counterparts. This update will provide a comprehensive overview of the Navy Federal scandal, shedding light on the claims and actions taken by various parties involved.

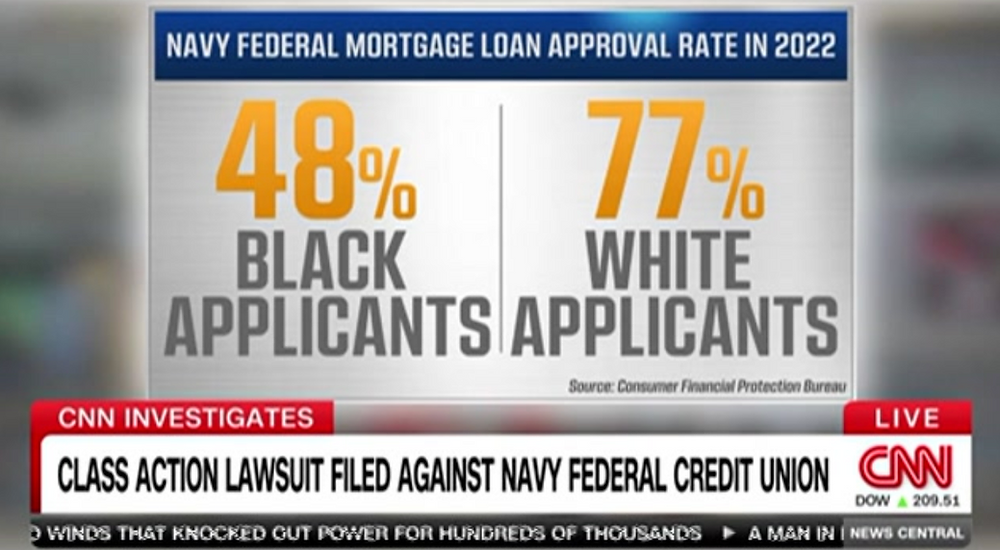

Understanding the Allegations

According to a report by CNN, Navy Federal Credit Union approved over 75% of white borrowers' applications for new conventional home purchase mortgages in 2022. However, less than 50% of Black borrowers who applied for the same type of loan were approved. This significant disparity raises concerns about racial discrimination in the credit union's lending practices.

Plaintiffs in the class-action lawsuits, such as Cherelle Jacob and Laquita Oliver, have alleged that Navy Federal rejected their home loan applications despite having excellent credit scores and substantial incomes. The lawsuits argue that these discriminatory practices violate the Fair Housing Act of 1968 and the Equal Credit Opportunity Act.

The Impact of Discrimination

The consequences of discriminatory lending practices are far-reaching, affecting individuals, families, and communities. Jerome Singletary, a U.S. Army veteran, and his family experienced the devastating effects firsthand. After being denied a home loan by Navy Federal, they struggled to find affordable housing and were forced to live in a shelter. This situation highlights the urgent need to address racial disparities in lending, as it can contribute to homelessness and perpetuate cycles of inequality. According to a report by qcnews, Mr.Singletary states: “We were denied because of our credit, and it was just a little hard for us. Things got really too complicated. So, we were forced to move into the shelter.” with followup questions by reporter Kaci Jones she ask: “Do you feel that if you were white, you would have been approved?”to which he responded:“Unfortunately, yes, I do. It’s sad to say, but yes”.

The Call for Accountability

Civil rights attorneys Benjamin Crump and Adam Levitt, known for their advocacy work, have taken a stand against Navy Federal Credit Union. They filed a class-action lawsuit on behalf of affected individuals, accusing the credit union of systematic discrimination in housing. The lawsuit demands accountability and seeks to shed light on the discriminatory practices allegedly employed by Navy Federal.

In response to the allegations, Navy Federal Credit Union released a statement expressing their commitment to addressing the issue. They have enlisted the expertise of Debo P. Adegbile, a leading civil rights lawyer, and his team to assess their mortgage lending policies and practices. The goal is to identify areas for improvement and drive further access to homeownership for all individuals, regardless of their race or ethnicity.

Who is Debo P. Adegbile

Debo P. Adegbile is an accomplished attorney, civil rights advocate, and legal strategist. He has dedicated his career to fighting for justice and equality. Adegbile holds a Juris Doctor degree from New York University School of Law and a Bachelor of Arts degree from Connecticut College.

Adegbile has an extensive background in civil rights law, having served as the Director of Litigation for the NAACP Legal Defense and Educational Fund (LDF) from 2001 to 2013. During his time at LDF, he successfully argued before the Supreme Court in several landmark cases, including the widely acclaimed case of Shelby County v. Holder, which addressed voting rights discrimination.

Adegbile's commitment to social justice and civil rights has earned him recognition and numerous accolades throughout his career. He has been a vocal advocate for criminal justice reform, fair housing, and voting rights. Additionally, Adegbile has served on various boards and committees dedicated to promoting diversity and inclusion within the legal profession.

Uncovering the Root Causes

While the focus is currently on Navy Federal Credit Union, it is crucial to recognize that racial disparities in lending extend beyond one institution. The housing industry as a whole must be held accountable for practices that perpetuate inequality. Representative Maxine Waters has emphasized the need for a comprehensive examination of industry practices, urging Congress to address the systemic issues that contribute to racial disparities in lending.

Innovating the Mortgage Process

To create lasting change, the mortgage industry must innovate and implement new practices that prioritize fairness and equal opportunity for all borrowers. One area where innovation is sorely needed is in credit scoring. Traditional credit scoring models, such as the classic FICO credit score, have been criticized for their potential to perpetuate racial biases. However, newer models like FICO 10T and VantageScore 4.0 aim to address these concerns and provide a more accurate assessment of creditworthiness.

Additionally, lenders should consider the unique circumstances and experiences of Black and Latino borrowers. Navy Federal Credit Union, as a membership organization serving government workers and veterans, should recognize the impact of applicants' military background and prioritize income as a predictor of loan repayment ability. By tailoring loan products and requirements to meet the needs of diverse communities, lenders can contribute to reducing racial disparities in mortgage approval rates.

FICO 10T Score

The FICO 10T Score is the latest credit scoring model developed by Fair Isaac Corporation (FICO), which is widely used by lenders to assess individuals' creditworthiness. This new scoring model introduces several key updates that aim to provide a more accurate and comprehensive representation of consumers' credit profiles.

One of the notable features of the FICO 10T Score is its incorporation of trended data. Unlike previous models that only considered a snapshot of consumers' credit information, the FICO 10T Score analyzes historical data over a 24-month period. This enables lenders to gain insights into borrowers' credit behaviors, such as their payment patterns and utilization rates over time, thus offering a more holistic view of their creditworthiness.

Moreover, the FICO 10T Score places greater emphasis on personal loans and credit card debt. It distinguishes between borrowers who consolidate their larger debts into personal loans and those who continue to accumulate credit card debt. This differentiation allows lenders to assess borrowers' behavior and risk more accurately, taking into account their ability to manage different types of credit effectively.

Another significant update introduced in the FICO 10T Score is a more nuanced approach to assessing credit risk for individuals who frequently participate in credit-seeking activities. This scoring model takes into account borrowers who exhibit higher levels of credit-seeking behavior, such as opening multiple accounts in a short period or applying for various credit products. By considering these factors, lenders can better evaluate consumers who frequently interact with credit and distinguish between responsible borrowing and higher risk behavior.

In summary, the FICO 10T Score aims to provide lenders with a more refined credit assessment tool, leveraging trended data, deeper analysis of personal loans, credit card debt, and enhanced evaluation of credit-seeking behavior. This new scoring model strives to offer a more accurate reflection of individuals' creditworthiness, helping lenders make informed decisions and borrowers access credit products that align with their financial circumstances and risk profiles.

Vantage Score 4.0

Vantage Score 4.0 is the latest iteration of the credit scoring model developed by the three major credit bureaus - Equifax, Experian, and TransUnion. Similar to the FICO models, the Vantage Score 4.0 aims to provide lenders with a comprehensive and reliable way to assess consumers' credit risk.

One key feature of the Vantage Score 4.0 is its ability to incorporate alternative data sources into the credit evaluation process. It considers non-traditional financial information, such as utility payment history, rent payments, and telecommunications accounts. This enables individuals with limited credit history, such as young adults or recent immigrants, to have a more accurate credit assessment by including additional data points beyond traditional credit accounts.

Another notable aspect of the Vantage Score 4.0 is its focus on trended credit data. Similar to the FICO 10T Score, this scoring model analyzes historical borrowing and repayment behaviors to better understand consumers' credit management habits over time. By considering trends, such as decreasing credit card balances or increasing credit utilization, the Vantage Score 4.0 offers lenders a more nuanced understanding of borrowers' creditworthiness.

Additionally, Vantage Score 4.0 incorporates machine learning techniques to enhance its predictive capabilities. This scoring model utilizes advanced algorithms to identify patterns and relationships within the credit data. By leveraging these techniques, the Vantage Score 4.0 can provide lenders with more accurate risk assessments, allowing them to make better-informed lending decisions.

Furthermore, Vantage Score 4.0 introduces a segmentation strategy that assesses consumers in specific credit-scoreable populations. This approach allows lenders to evaluate borrowers within specific population groups, such as millennials or immigrants, providing more targeted and relevant credit assessments for these subgroups.

The Vantage Score 4.0 continues to evolve and improve upon previous versions, aiming to provide lenders with a more comprehensive and inclusive credit scoring model. By incorporating alternative data, trended credit information, machine learning techniques, and population-specific evaluations, this model offers lenders a robust tool to assess credit risk accurately and promote financial inclusion for individuals with limited credit histories.

Promoting Financial Inclusion

Navy Federal Credit Union and its peers have an opportunity to lead the industry in promoting financial inclusion and challenging systemic inequalities. They can develop new loan products that address the disparate impacts reflected in racial disparities. For example, offering innovative insurance products that help homeowners make mortgage payments during income disruptions or unexpected expenses can contribute to sustainable homeownership and decrease delinquencies and foreclosures.

Refinancing can also be made more attractive to low-wealth borrowers, including Black and brown individuals, by offering automatic adjustments and providing support to help build credit scores. This can empower borrowers to take advantage of lower interest rates and improve their financial situations.

The Path Forward

The Navy Federal scandal serves as a wake-up call for the housing industry to address racial discrimination and promote equal access to homeownership. It is not enough to hold one institution accountable; the entire industry must commit to change. By implementing new mortgage products, assessing credit scoring practices, and fostering transparency, the industry can create a more equitable lending environment.

In conclusion, the Navy Federal scandal underscores the urgent need for reform in the housing industry. While the lawsuits against Navy Federal Credit Union seek justice for affected individuals, the systemic issues that perpetuate racial disparities in lending must be addressed industry-wide. By promoting financial inclusion, innovating mortgage practices, and prioritizing transparency, the industry can take significant strides towards a more equitable future.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered legal or financial advice. Please consult with a professional for personalized guidance.